Circle Files S-1: But What Are They Worth?

A deep dive into Circle's valuation

Note: This analysis was initially shared in The Weekly Stable (Vol 11): Circle files to go public on April 3rd 2025. It is being reshared here for easier linking.

Circle has officially filed its S-1. Headline numbers are $156M in net income on $1.68B of revenue.

There’s already great analysis out there on the Circle S-1 (see here, here, here, here, here and here). The key takeaway: most of the yield accrues to distributors like Coinbase and, as with many industries, value in stablecoins lies in distribution.

Rather than rehash the S-1 details, I want to focus on how to think about Circle’s valuation.

Most of the current discourse is centered around today’s metrics, revenue, margins, cost base, and the dominance of distribution. While these numbers help ground us in reality, valuation is about the future. Investors care about how these figures evolve and the probability-weighted range of outcomes.

Valuation 101

Early in my career, I spent my time evaluating companies when working in investment banking and private equity. There are many valuation methodologies, but they all boil down to the same thing: the present value of future cash flows.

Those future cash flows are driven by:

Growth of earnings – How much larger will the earnings stream become?

Quality of earnings – Are they repeatable, diversified, and cash-generative? Think: cash conversion, customer concentration, stickiness, recognition policies, cyclicality, competitive moat.

Once future earnings are estimated, they’re discounted using a rate that reflects the company’s cost of capital and investor risk appetite.

We won’t go deep into valuation mechanics here, but let’s walk through the key inputs to Circle’s valuation.

Growth Potential

The U.S. M2 money supply is ~$20T. The stablecoin market is only ~$230B. There's ample room to grow. The real question is: how much of that will USDC capture? And how much of the long term yield will they keep?

For 2024, Circle keeps 40% of the 5% yield they earn on USDC balances (average market cap of $33.3B) resulting in $659M gross profit. That’s roughly 200 bps on USDC market cap. In the long run, assume interest rates drop to 2% and Circle only retains 30 bps post-distribution in a more competitive market. At $500B in market cap, that’s still $1.5B in gross profit. At $1T, gross profit is $3B. Financial services are all about scale.

Net income (profit) potential scales depending on cost structure and operational leverage. At $1.5 - 3B of gross profit, a $1B+ net income business vs today’s $156M becomes plausible and potentially very attractive.

The stablecoin TAM is massive, and various scenarios can model different shares Circle might capture. Regulatory clarity helps Circle, but it also enables new entrants. Distribution remains critical for all competitors but Circle may have an edge with its partnerships plus early mover advantage. These distribution deals are expensive but necessary. They determine how defensible and scalable Circle’s earnings will be.

Quality of Earnings

Revenue concentration & rate sensitivity: 99% of revenue is interest income, which is highly sensitive to macro interest rate moves. With two rate cuts expected in 2025 and economic headwinds (e.g. tariffs, black swan risks), a downward trend in rates is more probable than not. No meaningful diversification in revenue = higher risk = lower quality earnings.

Cost structure: $263M in compensation but how does this scale? There is likely near-term growth needed to support compliance, BD, partnerships, regulatory affairs, blockchain development and so on, especially to grab and maintain share. However, it doesn’t necessarily grow with revenue or market cap. If distribution works as intended, revenue can scale much faster than costs. Over time, operating leverage will be critical for earnings growth.

Putting It All Together

At the end of the day, valuation is a supply-demand equilibrium between capital and opportunity. Circle is the only pure-play stablecoin company in public markets (or soon will be). That uniqueness may drive thematic capital interest but at the end of the day everyone will have to make their own determination.

Standard triangulation approaches apply—DCF, public comps, precedent transactions—but Circle doesn’t have great public comps/transactions. One way to reason through this is with a financial model:

Define plausible ranges for key variables

Test sensitivities

Assign probabilities

Arrive at a probability-weighted valuation

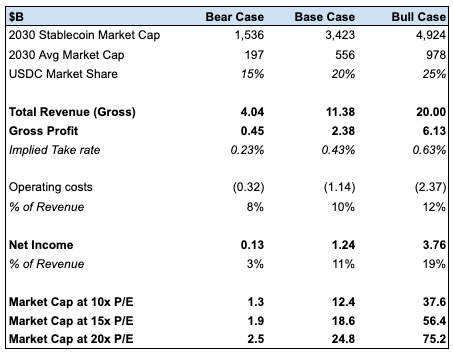

Sophisticated analysis will soon come from investment research departments of the investment banks covering the stock. However in the meantime I’ve built a simple model (nothing fancy—my ex IB colleagues would be embarrassed) to help you play with the assumptions and see how outcomes shift.

Base Case (2030):

Global stablecoin market: $3T

USDC share: drops from 25% to 20% → $556B

Take rate: 40 bps → $2.4B in gross profit

Operating costs: grow at 15% annually

Net income: $1.2B

2030 valuation at 10–20x P/E = $12B - $25B

Discount that back to today using your preferred rate, but if you believe those assumptions, $5B valuation at IPO might be very attractive.

2030 Bear Case:

USDC market cap stagnates

Take rate compresses to 20bps

OpEx grows, operating leverage doesn’t materialize

Net income collapses → valuation in low single-digit billions

2030 Bull Case:

USDC hits $1T in market cap (!)

Take rate expands to 60 bps

Operating leverage plays out

Earnings explode → high double-digit billion valuation

Of course, the devil's in the details and the details are in the assumptions.

Changes in each have varying degrees of effects on the model. Many more hours would be needed to build out sufficient detail to capture how the business will evolve. If you model nothing else, focus on these three:

Stablecoin market cap × USDC market share

Take rate (yield retained after distributor payouts)

Cost structure and leverage

Final Thoughts

Valuation is never about getting to a single number. It’s about understanding the range of outcomes and building conviction about the probability distribution. For potential Circle investors, I think the most important questions are:

How big is the stablecoin market in the long run?

What market share can USDC sustainably command?

How defensible is that share?

What’s the long-term take rate after accounting for distribution?

Can Circle maintain operating leverage?

What optionality exists for future revenue lines? (not modeled here)

Check out the model. Plug in your assumptions. See how your outlook translates into value.

Do you like the stock?

(Reminder: this is not financial advice)